Written by Anis Hadirah binti Abdul Mutalib and Poovarasan A/L Nalechami

Malaysia’s consumer credit sector has expanded rapidly with the growth of financial technology and alternative financing models. Services such as Buy Now Pay Later (“BNPL”) platforms, factoring and leasing, debt collection agencies and debt management services have become increasingly common, offering consumers greater access to credit and flexible payment options. However, many of these non-bank credit services previously operated under limited regulatory oversight, raising concerns regarding transparency, consumer protection, and responsible lending practices.

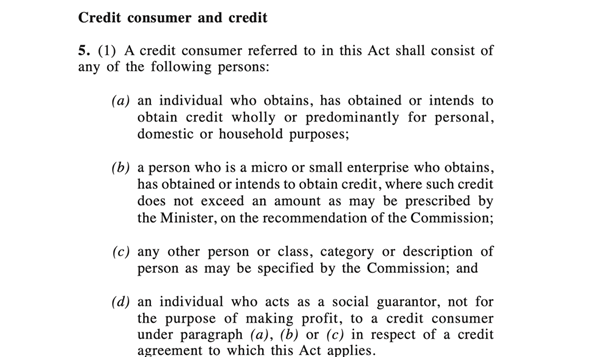

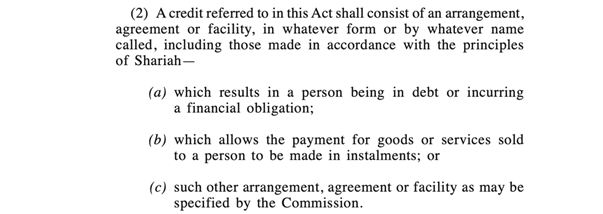

To address these regulatory gaps, the Malaysian government enacted the Consumer Credit Act 2025 (“the Act”)[1], which aims to establish a more comprehensive framework governing consumer credit activities. The Act was gazetted on 31st December 2025 and came into force on 1st March 2026. Under the new framework, credit providers such as BNPL platforms, leasing firms, and factoring companies are required to obtain licences in order to operate. In this regard, the Act also recognises the role of the consumer, whereby a ‘credit consumer’ is defines under Section 5 of the Act, thereby clarifying the category of persons to whom the Act applies in relation to consumer credit transactions[2].

Further, the establishment of the Consumer Credit Commission (“the Commission”) is a key feature of the Act, as it will regulate the consumer credit industry through clearer authorisation requirements, codes of conduct, and enforcement mechanisms. From the perspective of consumers, the introduction of the Act is expected to bring greater clarity and accountability in consumer credit transactions. Individuals who frequently utilise services such as BNPL providers, instalment payment platforms, or debt management services will now be dealing with credit providers that are subject to licensing requirements and regulatory supervision. This may lead to clearer disclosure of fees, repayment terms, and obligations before consumers enter into credit arrangements. Overall, the Act represents an important step towards strengthening governance within Malaysia’s credit industry while enhancing consumer protection in an increasingly digital financial environment.

PHASES

The implementation of the Act is designed to occur gradually through a structured phased approach. Each phase was introduced by the Consumer Credit Oversight Board which was established in 2021 to oversee the development and implementation of the new regulatory framework[3]. This strategy allows regulators, credit providers as defined under Section 4 of the Act[4], and consumers sufficient time to adapt to the new legal framework while ensuring that the transition towards a more comprehensive regulatory regime does not disrupt existing credit services.

The first phase focuses on preparation and the gradual introduction of regulatory requirements. During this stage, existing authorities continue to oversee their respective sectors while incorporating relevant consumer protection measures introduced under the Act. At the same time, the Commission begins establishing the necessary regulatory infrastructure, including licensing procedures, registration systems, and operational guidelines, pursuant to its powers under Section 8 of the Act to do all things necessary or convenient in connection with the performance of its functions[5]. As part of the early implementation measures, licensing rules for credit providers are set to take effect on 1st June 2026, after which BNPL providers and other credit providers will be given six months to comply with the licensing requirements.

The second phase involves the gradual transfer of regulatory functions to the Commission. During this stage, the Commission is expected to assume responsibility for overseeing various consumer credit activities that were previously regulated by different ministries and authorities. This consolidation is intended to create a more coordinated regulatory structure and improve consistency in the supervision of credit providers and service providers.

The final phase will complete the consolidation of consumer credit regulation under the Commission. At this stage, the Commission will function as the primary authority overseeing most consumer credit activities in Malaysia. The phased implementation therefore, reflects the government’s intention to ensure a smooth transition towards a unified regulatory framework while maintaining stability within the consumer credit industry.

CHANGES

One of the most significant changes introduced by the Act is the establishment of the Consumer Credit Commission, which can be seen under Sections 6 to 8 of the Act. These provisions set out the law relating to the establishment, functions and powers of the Commission. Section 6 of the Act[6] establishes the Commission as a body corporate with perpetual succession, while Section 7 of the Act[7] outlines the functions of the Commission, including advising the Government on national policy involving consumer credit and promoting proper conduct among credit providers and credit service providers. Meanwhile, Section 8 of the Act provides the Commission with broad regulatory powers, including the power to regulate and supervise credit businesses and credit service businesses.

The Commission will serve as the primary authority responsible for regulating consumer credit activities in Malaysia. Its role includes supervising credit providers, issuing licences pursuant to Section 42 of the Act[8], and ensuring that companies comply with the law. Previously, different agencies regulated different parts of the credit industry. However, with the creation of the Commission, oversight will be centralised and a more consistent regulatory system will be established. For the public, this means there will be a dedicated authority responsible for protecting consumers in the credit market. This framework also ensures that only qualified and responsible companies are allowed to provide credit services. For instance, Section 40 of the Act[9] requires any person carrying on a credit business to obtain a licence, failing which the person commits an offence. Companies that fail to meet regulatory standards may therefore face penalties or even lose their licence.

The Act also emphasises transparency in credit transactions. Credit providers must clearly disclose important information to consumers such as the total cost of borrowing, interest rates and fees, payment schedules, and most importantly, late payment charges. This requirement is reflected in the business conduct provisions under Sections 84 and 85 of the Act, which require credit providers and credit service providers to conduct their business in a fair, responsible and professional manner when dealing with credit consumers. In particular, Section 85 of the Act[10] allows regulations and guidelines to impose transparency and disclosure requirements to ensure that information provided to consumers is accurate, clear and not misleading.

Consumers will therefore have a clearer understanding of what they are agreeing to before taking on a loan or credit facility. This change is particularly important for BNPL services, which are often marketed as quick and convenient payment options. While these services may appear simple, they still involve borrowing money and must be used responsibly. By requiring clearer disclosures, the law aims to help consumers make more informed financial decisions.

Another major change introduced by the Act is the promotion of responsible lending practices. Credit providers will be required to follow conduct standards set by the Commission. As mentioned earlier, Section 84 of the Act[11] imposes a duty on credit providers to ensure fair, responsible and professional business conduct, while Section 85 of the Act further allows regulations to require assessments of the affordability of credit offered to consumers before credit is granted. This is important because excessive borrowing can lead to serious financial problems for individuals and families. When lenders fail to properly assess a borrower’s financial ability, consumers may end up trapped in debt. Responsible lending rules therefore help ensure that credit providers do not encourage irresponsible borrowing simply to increase profits.

Furthermore, debt collection practices have long been a concern for many borrowers. Some debt collectors have been accused of using aggressive or unethical tactics when attempting to recover debts. The new Act seeks to address this issue by regulating credit service providers and establishing standards governing debt collection practices. In particular, Section 85(1)(g) of the Act[12] allows regulations and guidelines to impose requirements relating to fair debt collection practices, ensuring that credit providers and credit service providers treat borrowers fairly during the debt recovery process. With proper oversight, debt collectors must operate within legal and ethical boundaries. This ultimately protects borrowers from harassment or unfair treatment while still allowing legitimate debts to be recovered.

Beyond regulation, the Act may also encourage greater financial awareness among Malaysians. The Act recognises the importance of consumer protection and financial education in building a responsible credit culture. For example, the Advisory Committee established under the act plays a role in promoting credit consumer awareness and financial education to encourage a sound credit culture. As credit providers are required to provide clearer information and follow stricter standards, consumers may become more aware of the risks associated with borrowing. In the long run, this could lead to a healthier financial culture where individuals make more responsible borrowing decisions.

The Act marks an important step in modernising Malaysia’s consumer credit framework. By introducing stronger regulation, establishing the Consumer Credit Commission and bringing emerging credit services under federal oversight, the Act aims to protect consumers while promoting a fair and transparent credit industry.

From the perspective of consumers, the Act is expected to have a direct impact on how individuals interact with credit providers. Users of credit services, including those who rely on personal loans, instalment facilities and BNPL platforms, will likely experience greater transparency when entering credit arrangements. Credit providers will be required to provide clearer information regarding interest rates, fees, repayment schedules and potential penalties. As a result, consumers will be in a better position to understand the true cost of borrowing before committing to a financial obligation.

In addition, the regulation of previously less regulated sectors such as BNPL services and debt collection agencies may improve consumer confidence in the credit market. Consumers who face financial difficulties may also benefit from clearer standards governing responsible lending and debt collection practices. These measures can help ensure that borrowers are treated fairly and are not subjected to misleading information or aggressive collection methods.

However, the new regulatory framework may also lead to stricter assessment procedures by credit providers when approving loans or credit facilities. While this may make it slightly more difficult for some individuals to obtain credit quickly, it ultimately encourages more responsible borrowing and reduces the risk of excessive household debt. In the long term, such measures are likely to contribute to greater financial stability for individuals and families.

Ultimately, the Act represents a significant move toward a safer and more sustainable credit environment for Malaysian society. By strengthening consumer protection while encouraging responsible lending practices, the Act aims to strike a balance between accessibility to credit and the financial well-being of consumers.

Dated : 17 March 2026

[1] Act 873

[2] Section 5 of the Act

[3] https://ccob.my/about/

[4] Section 4 of the Act

[5] Section 8 of the Act

[6] Section 6 of the Act

[7] Section 7 of the Act

[8] Section 42 of the Act

[9] Section 40 of the Act

[10] Section 85 of the Act

[11] Section 84 of the Act

[12] Section 85(1)(g) of the Act